With inflation running hot, real estate is a refuge

Real estate investing

10/24/2022

Written by Tom Brady

Reviewed by Mynd Editorial Staff

Federal Reserve chairman Jerome Powell and his colleagues raised short-term interest rates by 75 basis points on November 2 in an effort to cool inflation, which creeped past 9 percent in June, its highest rate in 40 years. It fell to 8.2 percent in September.

This was the fourth 75 basis point hike in as many Fed meetings, bringing the Fed's baseline interest rate range to a span of 3.75 to 4 percent. Officials expect to continue raising rates in 2023.

The Fed's increased rate chiefly affects the cost of borrowing for items like credit cards, car financing, and adjustable rate mortgages.

What happens to real estate during inflation? Housing prices rise, so real estate investors see appreciation. Upward pressure on prices means that longtime owners have recently seen a steep rise in the value of their assets. Also, mortgage payments do not change over time, but money paid back in the future is worth less. Inflation has also driven up rents.

Mortgage interest rates have risen along with inflation, with the rate on a 30-year fixed mortgage reaching about 7 percent. As recently as December, that rate was just over 3 percent.

Higher interest rates, coupled with pandemic-fueled price increases, have caused affordability issues in some of the high-flying markets around the country, but prices have begun to fall in markets nationwide as many would-be homebuyers find they can't afford the higher monthly payments dictated by rising interest rates.

Few experts predict that home prices will fall substantially, even as the Fed raises short-term rates and sells off some of its balance sheet to bring inflation under control, which the Fed chief says is a top priority.

Powell conceded that a recession is possible, after previously maintaining he was aiming for a "soft landing," reducing inflation without killing growth.

Many economists said the Fed waited too long to address inflation, but Powell was concerned about attaining full employment in the economy. Wages rose, and many employers complained about finding workers, but some expect joblessness to increase as fears of a recession loom.

As inflation spikes and the Fed raises rates to try to cool it, higher mortgage rates have cooled housing markets in some parts of the country. (Getty Images)

How is real estate a hedge against inflation?

Investing in real estate offers a couple of advantages during inflationary periods, and this recent runup is no exception. And there is scads of evidence that a diversified portfolio, one that has 20 percent or more invested in real estate, offers strong and stable returns.

Doug Brien, the CEO of Mynd, believes an inflationary environment creates more opportunities for investors in the SFR market.

“It's an attractive option because rents are bound to rise along with inflation,” Brien said, which increases the cash flow for property owners.

As interest rates rise in an inflationary environment, demand for rental homes is likely to increase as well, he added.

“If it becomes more expensive for potential buyers to finance a purchase, fewer will be able to afford it,” Brien said. “This will increase demand for single family homes and create more upward pressure on rental prices.”

How do mortgage rates correlate to inflation?

Short-term inflation generally has little impact on mortgage rates, which are more closely linked to the 10-year Treasury bill, where rates tend to rise slowly.

The interest rate the Fed controls is what banks and credit unions use to lend to each other overnight. This is a very different lending market than the one for mortgages, where banks compete with one another for business.

As of late October, the rate on the 10-year T-bill has reached 4.21 percent. In March, it was hovering around 2 percent, but as recently as early December the yield was at 1.35 percent.

Mortgage rates have been following the Treasury bill, rising steadily since the end of last year. For most of 2021, 30-year mortgages could be had for around 3 percent, and refinance activity was robust as many homeowners rushed to take advantage of the lower rates.

Mortgage lenders have seen major rounds of layoffs in response to the fall in demand for loans and refinancing as rates have risen.

Though the average rate had reached above 7 percent as of late October, more than double the historic lows reached earlier in the pandemic, in a historical perspective, the current number still qualifies as low. (While the 30-year rate has typically stayed below 10 percent since 1971, it did spike to 18.53 percent in October 1981.)

As rates for primary residences rise, the impact on borrowing for investors in the single family residential (SFR) sector is softened by the fact that they're already paying higher rates than homeowners. And owning property brings with it numerous benefits.

“Even in this crazy environment, property is still a relatively safe investment,” said Dennis Bron, vice president of growth for Mynd.

SFR investors earn cash from collecting rent, and owners who buy and hold are able to employ several strategies to reduce their tax burden, writing off many expenses associated with a rental property, and taking depreciation on a home.

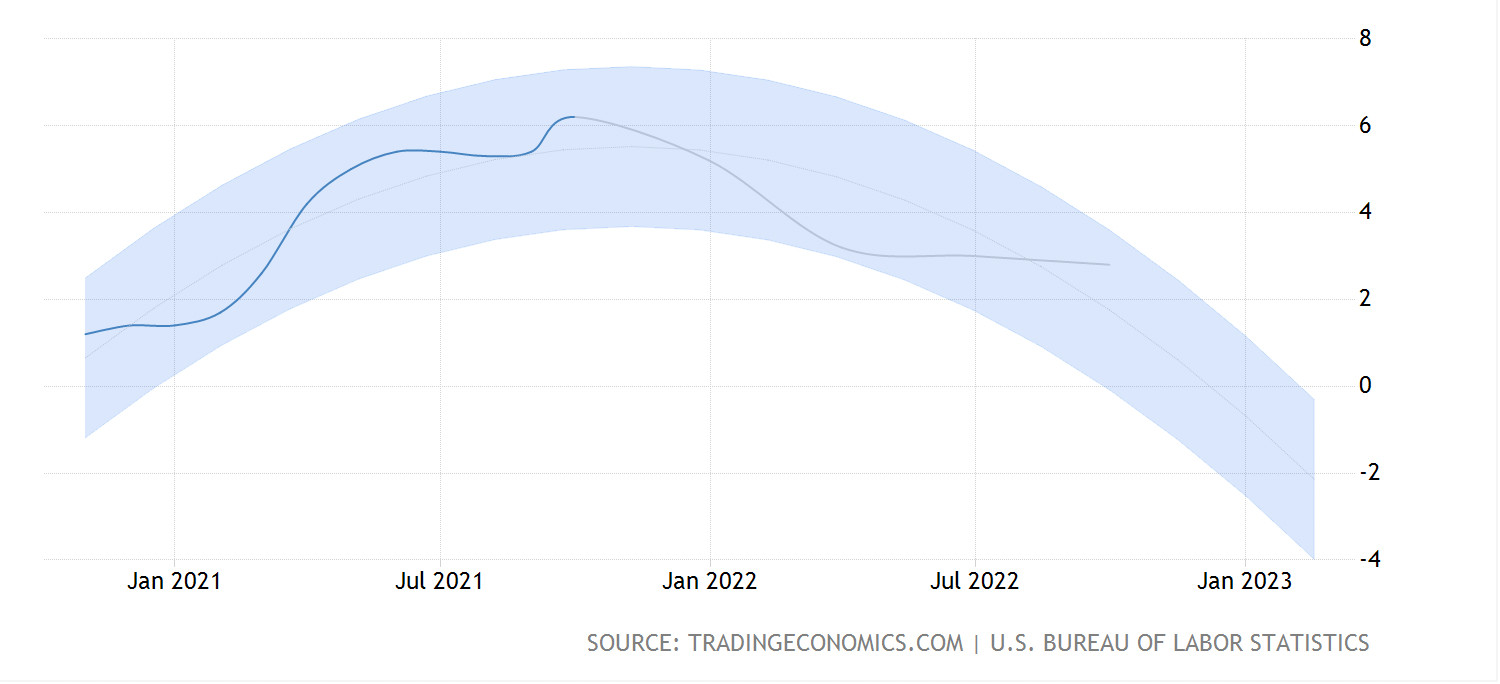

Inflation hit 6.2 percent year over year in October, its highest rate since 1990. (tradingeconomics.com/U.S. Bureau of Labor Statistics)

Concerns about jobs drove Fed policy

For most of 2021, Powell and his colleagues at the Fed expressed their concerns about the job market, and were reluctant to make any moves that would prevent the economy from reaching full employment. (The unemployment rate was 3.8 percent in February; it peaked at 14.7 percent in April 2020, the height of the pandemic.)

Frederic Mishkin, a Columbia University professor and former Fed governor, said in December that the economy had already reached full employment and the Fed was “much too optimistic on the inflation front,” and distracted by its focus on the labor market.

Mishkin said then that he feared the Fed would have to raise rates higher than it would otherwise need to if it had acted earlier.

“The Fed is behind the curve,” Mishkin said in an interview with CNBC back in December. “The reality is that inflation is higher than they anticipated and it's more permanent than they anticipated.”

Professor Mishkin was prescient, as the economy has hit the highest inflationary levels since the Reagan Administration.

Housing market's rise preceded inflation surge

The increase in home prices started before recent inflationary pressures, as a shortage of homes, and the pandemic-fueled migration to the suburbs and smaller cities, spurred bidding wars and double-digit-percentage hikes in home prices in many cities.

These increases hit families looking to buy in the SFR space, as well as investors, a group that now includes some deep-pocketed institutions like JP Morgan, Blackstone and the Toronto-based investment firm Tricon Residential, which plans to invest $5 billion in single family rental homes in the U.S. in partnership with Teacher Retirement System of Texas and Pacific Life Insurance Company.

John Burns Real Estate Consulting estimated that some $45 billion in institutional money flowed into the SFR and build-to-rent sectors in 2021.

Many observers of the housing market are trying to figure out the direction the market will take as the reality of higher mortgage rates settles in. Cities like Atlanta, Phoenix, Raleigh, Charlotte, Tampa and Austin saw double-digit percentage increases over the last three years, but the increase in rates has slowed the housing market.

Some markets, like Phoenix, have seen a correction in the second half of 2022. Others, like Austin, are experiencing something more like a flattening, as demand is not expected to fall off dramatically given the number of jobs (mostly in technology) migrating there.

Many experts believe that there are still good opportunities, if investors do their homework and find properties that have potential.

“Rental housing demand is going to continue,” said Don Ganguly, senior vice president of Mynd Investment Management. "Some percentage of people are going to work out of their houses for some period of time. A lot of those people may not want to buy, so you are going to have a spillover from the apartment rental cohort who are looking for a home in the rental market.”